ahead of earnings! Strong growth momentum in advertising business, but hefty spending guidance may raise concerns.")

In its report, Deutsche Bank assigned a ‘Buy’ rating to Meta with a price target of $880, which represents an upside potential of approximately 34% from the stock’s closing price last Friday.

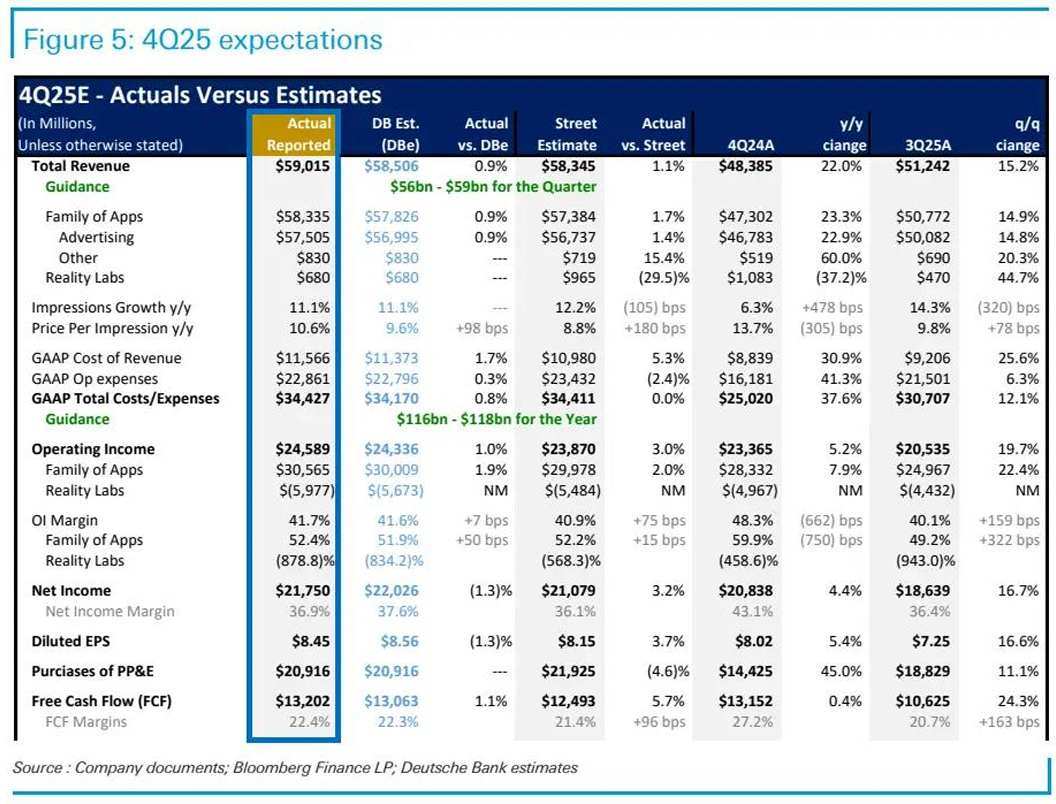

According to Zhitong Finance APP, Meta Platforms (META.US) will announce its Q4 2025 earnings after the U.S. stock market closes on January 28 (Wednesday). Deutsche Bank issued a report stating that it expects Meta’s Q4 revenue to reach $59 billion (a year-on-year increase of 22%), higher than the previously estimated $58.5 billion; the expected total expenditure for Q4 is $34.4 billion, which would place the full-year total expenditure at the midpoint of the company’s projected range of $116-118 billion. For Q1 2026, Deutsche Bank forecasts revenue to grow by 23% year-on-year to $51.9 billion, compared to the market consensus expectation of $51.2 billion; total expenditures are expected to grow by 32% year-on-year to $32.6 billion, versus the market consensus estimate of $33.1 billion. In its report, Deutsche Bank assigned Meta a ‘Buy’ rating with a target price of $880, representing an approximately 34% upside from the stock’s closing price last Friday.

Deutsche Bank stated that Meta’s guidance for total expenditure and capital expenditure in 2026 will be a clear focal point. The bank’s communications with buy-side institutions indicate an expectation of Meta’s total expenditure in 2026 to be between $150-160 billion, with capital expenditure forecasted at $120-130 billion.

![]()

Channel checks indicate that revenue growth is likely to remain robust.

Deutsche Bank noted that in a recent call with Andrew McLean, Head and Managing Director of Inventus Media, a consulting and research firm focused on the media/entertainment industry, he observed, based on his company’s advertising spending trends, that digital ad spending grew by more than 9% year-on-year in Q4 2025, accelerating from 8.3% in Q3 and 7% in Q2. This was primarily driven by improvements in return on investment (ROI) from AI-based initiatives by Meta and Google, which account for approximately 60% of its digital ad spending.

McLean pointed out that since early 2025, overall ad spending, including traditional media, has been growing at twice the rate of GDP growth. This is mainly due to the tangible benefits of AI in enhancing data analytics, leading to better targeting and automated creative generation. As a result, platforms like Google and Meta saw their ROI increase by 6.8% and 9% respectively in Q4 2025, compared to the historical average annual increase of 2%. McLean also emphasized that Meta is one of the few platforms fully leveraging its AI capabilities across its entire AI infrastructure.

Key performance indicators for engagement continue to show positive trends.

According to Sensor Tower, the total usage time of Meta’s Facebook and Instagram applications continues to grow at an accelerated pace. This is driven by Instagram’s expanding user base, improving trends for Facebook, and increasing daily engagement. Since Q4 2024, the strong growth in engagement has been particularly noticeable, reflecting continuous improvements in Meta’s recommendation system in providing personalized content to users.

Ad impressions and eCPM (earnings per thousand impressions) both grew at healthy double-digit rates.

Advantage+ is a set of AI-powered fully automated end-to-end marketing solutions launched by Meta, designed to help businesses streamline ad placements and enhance effectiveness. Deutsche Bank noted that as Advantage+ becomes the default campaign setting for more advertisers and continuous improvements are made to the ad tech stack, the bank sees AI enhancements increasingly manifesting in the form of improved returns on ad spend.

Deutsche Bank still expects this to become a lasting growth driver for Meta in the future, particularly due to: 1) Andromeda – Meta’s AI-powered ad retrieval engine – which has yet to be fully rolled out in Instagram feeds and Reels; 2) GEM – Meta’s generative advertising model – which enhances the ability of other ad recommendation models to deliver relevant ads, thereby improving ad performance and advertisers’ return on investment. Further improvements are anticipated as the model will be trained using larger GPU clusters by 2026 and expanded to Facebook Reels; 3) Lattice – the ad ranking architecture – where model simplification remains a source of improved return on ad spend.

Therefore, it is unsurprising that Northbeam data shows Meta maintaining strong market share. With conversion growth outpacing impression growth, Deutsche Bank is optimistic that better return on ad spend and a very healthy cost-per-action trend will lead to greater ad budget allocations in the near-to-medium term.

Deutsche Bank raises revenue growth and operating expense forecasts

Deutsche Bank stated that, based on stronger-than-expected momentum in Q4 2025 and a weaker US dollar, it raised its revenue forecast for Meta’s Q4 by approximately 1% to USD 59 billion. The bank still believes that revenue from the Reality Labs division may decline by double digits year-over-year in Q4, likely due to the absence of new headset launches and retailers restocking, which shifted some revenue to Q3 2025.

Deutsche Bank also revised upward its estimate for Meta’s Q4 ad revenue growth from 22% to 23% year-over-year. Based on this, the bank believes the market may revise upward Meta’s 2026 ad revenue growth forecast from the current 18%. In the medium term, Meta will benefit from performance improvements in its advertising and recommendation infrastructure.

Nevertheless, concerns persist regarding the potential impact of Meta’s apps launching non-personalized ad versions in the EU region (mandated by the Digital Markets Act). Although Meta may seek amendments, the outcome remains uncertain given ongoing geopolitical issues. Therefore, for 2026 and 2027, Deutsche Bank made slight upward adjustments to its forecasts to reflect sustained strength in core advertising operations.

Moreover, despite Meta’s recent disclosure of a 10% workforce reduction in the Reality Labs division, Deutsche Bank believes that spending growth in 2026 could slightly exceed its prior projections, driven by: 1) higher infrastructure expenditures, including greater public cloud spending, increased energy costs, and higher depreciation and amortization; 2) personnel-related costs stemming from investments in generative AI and superintelligence labs. Meta’s off-balance-sheet commitments rose to approximately USD 140 billion in Q3 2025, reflecting its focus on upfront investments in AI. As Meta begins executing leases already included in these commitments, Deutsche Bank anticipates a significant increase in reported lease costs and liabilities in 2026. Over the long term, with more self-built data centers coming online, depreciation and amortization growth may accelerate.

link