Europe Digital Advertising Market Size, Share & Growth 2033

Europe Digital Advertising Market Size

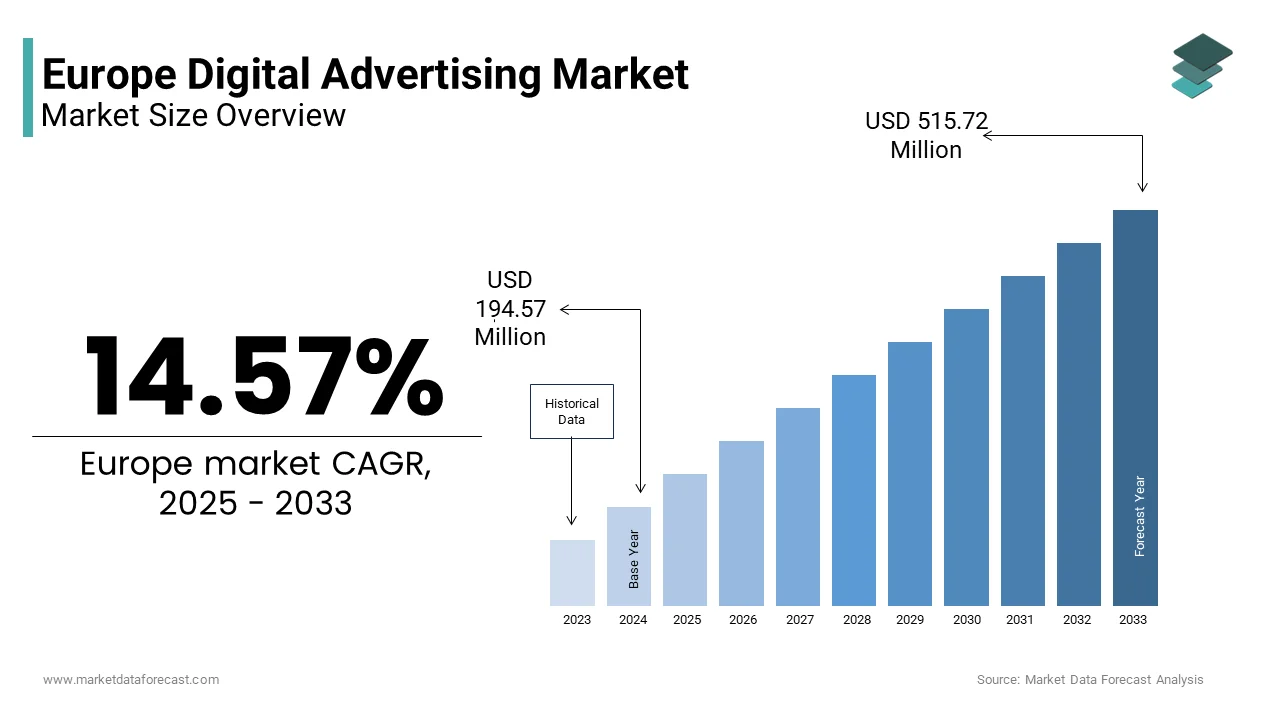

The Europe digital advertising market was valued at USD 169.71 million in 2024 and is anticipated to reach USD 194.57 million in 2025 to USD 515.72 million in 2033, growing at a CAGR of 14.57% during the forecast period from 2025 to 2033.

The Europe digital advertising market encompasses the deployment of paid promotional content across digital channels such as search engines, social media platforms, display networks, video streaming services, and mobile applications to reach targeted audiences within the European region. Unlike traditional advertising, digital advertising leverages real-time data analytics, behavioral tracking, and programmatic buying to optimize ad delivery and performance. The market operates within a complex regulatory environment shaped by the European Union’s stringent data protection laws, notably the General Data Protection Regulation. Digital ad formats include search ads, display banners, native advertising, social media promotions, and connected TV spots. According to the European Commission, a large majority of European internet users engage with digital content daily, creating a fertile ground for precision-driven advertising strategies. According to Eurostat, in 2024, most individuals aged 16 to 74 in the European Union accessed the internet at least once a week, and many used mobile devices as their primary means of online access. Furthermore, according to the International Telecommunication Union, fixed broadband download speeds across Western Europe have continued to rise, enabling seamless delivery of rich media advertisements. These foundational digital infrastructure and behavioral metrics underpin the operational dynamics of the Europe digital advertising ecosystem.

MARKET DRIVERS

Accelerated Mobile Internet Penetration Fuels Precision Targeting Capabilities

The proliferation of high-speed mobile internet across Europe has fundamentally reshaped digital advertising by enabling real-time, location-based, and context-aware ad delivery. Mobile devices now serve as the primary gateway for digital content consumption, allowing advertisers to deploy hyper-targeted campaigns that respond to user behavior in milliseconds. According to the European Electronic Communications Observatory, most European households had access to 5G coverage by the end of 2024, significantly expanding the bandwidth and responsiveness of mobile advertising ecosystems. This infrastructure advancement supports richer ad formats such as interactive video, augmented reality overlays, and shoppable media, which demand low latency and high throughput. According to the GSMA Intelligence report published in March 2025, mobile data traffic in Europe grew substantially year on year, reaching higher average usage per smartphone per month. This surge in mobile engagement has prompted advertisers to reallocate budgets toward in-app and mobile web placements. According to the German Association of the Digital Economy, mobile advertising accounted for a major share of total digital ad spend in Germany in 2024. The convergence of dense 5G networks, rising smartphone ownership, and evolving consumer expectations for personalized experiences has thus created a self-reinforcing cycle that intensifies demand for mobile-centric programmatic advertising solutions across the region.

Rising Adoption of E Commerce Platforms Drives Performance-Based Advertising Demand

The structural shift toward online retail across Europe has intensified reliance on performance-oriented digital advertising, where success is measured through conversions, click-through rates, and return on ad spend. As consumers increasingly favor digital storefronts for convenience and variety, brands must compete for visibility in crowded search and social feeds, necessitating sophisticated bidding and attribution strategies. According to the European digital statistical sources, e-commerce activity in the EU is continuing to grow. This growth is particularly pronounced in certain parts of Southern and Eastern Europe, where online retail penetration is rising faster than the overall union average. According to the “Digital Economy and Society Index” framework published by the European Commission, a substantial share of European enterprises are now making goods or services available online. This expansion has amplified demand for search-engine marketing and dynamic product ads that automatically adjust based on inventory and user intent. Retailers are increasingly allocating a major portion of their marketing budgets to digital channels, with a significant focus on performance-oriented media such as Google Shopping and Meta’s conversion-optimised campaigns. The symbiotic relationship between e-commerce growth and measurable advertising outcomes continues to propel investment in data-driven ad technologies across the continent.

MARKET RESTRAINTS

Stringent Data Privacy Regulations Constrain Behavioral Targeting Mechanisms

The European Union’s robust data protection framework, anchored by the General Data Protection Regulation, imposes significant limitations on the collection, storage, and utilization of personal data for advertising purposes, which is one of the major restraints to the growth of the European digital advertising market. These constraints directly impede the functionality of behavioral targeting, which relies on tracking user activity across websites and apps to build interest-based profiles. According to CMS Law’s GDPR Enforcement Tracker, cumulative data-protection fines across EU member states reached approximately €5.88 billion by January 2025. The phasing out of third-party cookies by major browsers further compounds this challenge. According to Google’s own blog post, in December 2023, the Google Chrome browser began restricting third-party cookies for a small test group of users as part of its Privacy Sandbox initiative. The technical shift has eroded the accuracy of cross-site tracking by forcing advertisers to rely on less precise contextual or cohort-based alternatives. According to the latest reports, third-party cookie removal has found that retargeting campaign effectiveness was noticeably reduced in several European countries. Consequently, many small and medium-sized enterprises report declining return on ad spend as they lack the resources to implement compliant first-party data strategies or invest in privacy-preserving identity solutions. The regulatory environment, while essential for consumer rights, continues to impose structural friction on the scalability and efficiency of digital advertising operations in Europe, which is negatively impacting the growth of the European digital advertising market.

Fragmented Regulatory Landscape Across Member States Increases Compliance Complexity

Despite the harmonizing intent of EU-wide legislation, divergent interpretations and enforcement practices among member states create a patchwork of compliance requirements that complicate pan-European advertising campaigns and hinder the growth of the European market. National data protection authorities often issue conflicting guidance on issues such as cookie consent mechanisms, legitimate interest assessments, and cross-border data transfers, which is leading to operational uncertainty for advertisers. Enforcement actions related to digital advertising by European Data Protection Authorities have increased significantly in recent years, and this has resulted in multi-billion-euro fines. The phasing out of third-party cookies by major browsers further compounds this challenge. According to recent reports, the removal of third-party cookies has materially reduced the effectiveness of retargeting campaigns in key European markets.

MARKET OPPORTUNITIES

Expansion of Connected TV and Addressable Advertising Opens New Inventory Avenues

The rapid migration of television viewership from linear broadcast internet-connected platforms has unlocked high-impact, brand-safe advertising inventory previously inaccessible to digital buyers, which is one of the significant opportunities in the European digital advertising market. Connected TV now enables advertisers to deliver personalized ads within premium video content while maintaining the immersive and full-screen experience associated with traditional television. Streaming platforms have become integral to entertainment consumption across Europe, with household adoption and viewing hours continuing to rise steadily. This shift has catalyzed investment in addressable TV advertising that allows different households to receive distinct ads during the same program based on demographic or behavioral data. Addressable TV ad spend in Europe has recorded strong year-on-year growth, which reflects increasing adoption among broadcasters and advertisers. Markets such as the United Kingdom, France, and Sweden lead adoption with broadcasters like Sky, TF1, and Viaplay offering programmatic access to segmented audiences. Unlike open web display ads that often suffer from viewability and fraud concerns, connected TV offers high completion rates and strong brand lift metrics. Advertisers widely consider connected TV a highly trustworthy channel for premium brand messaging. As infrastructure matures and measurement standards converge, this channel is poised to absorb a growing share of brand budget allocations by offering a scalable alternative to saturated social and search environments.

Integration of Artificial Intelligence Enhances Creative Optimization and Media Buying Efficiency

The deployment of generative and predictive artificial intelligence tools is transforming both the creative and operational dimensions of digital advertising in Europe, which is another promising opportunity in the European market. AI-powered platforms now enable real-time generation of ad variants, dynamic copy personalization, and predictive bid optimization based on probabilistic user response models. AI adoption in marketing across Europe has been expanding rapidly, with large enterprises increasingly integrating it into their technology stacks. These systems analyze vast datasets, including historical campaign performance, weather patterns, local events, and economic indicators that adjust messaging and media allocation with minimal human intervention. AI-driven creative platforms can produce thousands of banner or video ad permutations tailored to micro segments, which significantly improves engagement rates. On the media buying side, machine learning algorithms reduce wasted impressions by identifying high-propensity audiences with greater accuracy than rule-based systems. AI-optimized campaigns have demonstrated higher returns on ad spend across sectors such as retail and automotive, which reflects growing confidence in automated decision-making. Crucially, these technologies operate within privacy-preserving frameworks such as federated learning and allow performance gains without violating data minimization principles. As computational capabilities advance and regulatory sandboxes expand, AI is set to become the central nervous system of the European digital advertising market.

MARKET CHALLENGES

Persistent Ad Fraud and Invalid Traffic Undermine Campaign Integrity and ROI

Despite technological countermeasures, non-human traffic and sophisticated fraud schemes continue to distort performance metrics and drain advertiser budgets across the European digital ecosystem, which is primarily challenging the expansion of the European market. Invalid traffic, such as including bots, click farms, and domain spoofing, generates false impressions and clicks that inflate reported engagement while delivering no real audience reach. Digital ad fraud continues to be a significant challenge across Europe and resulting in substantial losses for advertisers. The problem is particularly acute in open programmatic exchanges where opaque supply chains enable fraudulent publishers to masquerade as premium inventory. Audits have shown that a considerable share of domains in the long-tail programmatic marketplace exhibit bot-driven traffic patterns inconsistent with human behavior. Mobile in-app advertising remains especially vulnerable to fraudsters exploiting SDK spoofing techniques to simulate app installs and post-install activity. Mobile app install fraud in Europe has been rising year on year and disproportionately affecting gaming and fintech advertisers. While verification tools from accredited vendors can mitigate some risks, their adoption remains inconsistent among small and mid-sized advertisers due to cost and complexity. The persistent presence of economically motivated fraud actors thus erodes trust in digital channels and complicates accurate performance attribution across the region.

Declining Consumer Trust and Rising Ad Blocker Usage Diminish Reach and Engagement

European consumers are increasingly skeptical of digital advertising practices, which is contributing to the widespread adoption of ad-blocking tools and reduced interaction with promotional content, and this is further challenging the regional market growth. This erosion of trust stems from perceptions of intrusiveness, data exploitation, and irrelevant messaging that collectively diminish the effectiveness of even well-targeted campaigns. Ad blocking has become a widespread behavior among internet users in the European Union, with adoption particularly high in countries such as Germany and the Czech Republic. The prevalence of disruptive ad formats such as auto-playing videos, pop-ups, and interstitials continues to fuel user frustration and avoidance behaviors. Many European users report abandoning websites due to excessive or poorly placed advertisements. This behavioral shift directly impacts campaign reach as blocked impressions never contribute to brand awareness or conversion funnels. Moreover, ad blocking correlates strongly with higher digital literacy, which means that the most valuable, tech-savvy audiences are often the least reachable through conventional display strategies. While some publishers have implemented acceptable-ads programs or paywall alternatives, these measures have achieved limited success in restoring engagement. Without a fundamental recalibration toward user-centric, value-exchanging ad experiences, the gap between advertiser intent and consumer receptivity will continue to widen across the European digital landscape.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2024 to 2033 |

|

CAGR |

14.57% |

|

Segments Covered |

By Platform, Format, Offering, Type, End-User, and Country |

|

Various Analyses Covered |

Regional and Country-Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

Germany, the UK, France, Spain, Russia, Sweden, Denmark, Italy, Switzerland, the Netherlands, and the Rest of Europe. |

|

Market Leaders Profiled |

Adobe, Amazon.com Inc., AOL (Yahoo)M Baidu, Byte Dance, Dentsu Inc., Disruptive Advertising, Global, IAC, Meta, Microsoft Corporation, Tencent Holdings Ltd., Verizon, Web FX, X Corp. (formerly Twitter Inc.) |

SEGMENTAL ANALYSIS

By Platform Insights

In 2024, the smartphone-based digital advertising segment occupied 67.5% of the regional market share. This overwhelming dominance of the smartphone segment is mainly due to the two interlinked structural shifts in consumer behavior and technological infrastructure. Pervasive mobile device ownership and daily usage patterns are also boosting the expansion of the smartphone segment in the European market. Smartphones have become the default digital interface for European consumers anare d are fundamentally altering how advertising inventory is consumed and monetized. Smartphone ownership among individuals aged 16 to 74 in the European Union was high, and average daily screen time on devices exceeded several hours. This deep integration into daily routines enables advertisers to reach users during high-intent moments such as commuting, shopping, or social interaction, where responsiveness to ads is significantly higher. Mobile devices generated a large majority of web traffic across Europe in recent years, with a noticeable increase between 2022 and 2024. Advertisers have responded by prioritizing mobile-first creative strategies, with mobile-optimized landing pages and vertical video formats now standard practice. In Germany, a strong majority of online purchases started via digital ads were traced to smartphone users, which confirms the commercial strength of mobile channels. This behavioral entrenchment ensures that smartphone advertising remains the primary conduit for performance and brand campaigns alike and propels the further expansion of the smartphone segment in the European market.

By Format Insights

The video advertising segment led the market by holding 46.4% of the European digital advertising market share in 2024. The unmatched ability to convey narrative, emotion, and product demonstration in a single impression and consumer preference for immersive, story-driven content are majorly driving the growth of the video advertising segment in the European market. European audiences increasingly favor video as their primary mode of digital content consumption, which is creating natural alignment with advertiser objectives. According to the European Audiovisual Observatory, users across Europe spend considerable time each week on video streaming platforms, with short-form video on platforms like TikTok and Instagram Reels accounting for a large share of total engagement. This shift has prompted brands to prioritize video storytelling, particularly in sectors such as fashion, automotive, and travel, where visual demonstration is critical. According to a 2024 survey, consumers recalled video ads more accurately than static formats, and many reported higher purchase intent after watching a product video. Skippable in-stream video ads have achieved strong completion rates when content is relevant, far exceeding banner click-through averages. This psychological and behavioral resonance ensures video remains the format of choice for both brand building and performance campaigns, and drives the growth of the video advertising segment in the European market.

By Offering Insights

The solutions segment had 2.6% of the European digital advertising market share in 2024. The leading position of the solutions segment in the European market is primarily attributed to the growing enterprise demand for integrated, self-serve advertising infrastructure. Large advertisers and agencies increasingly prefer end-to-end software solutions that enable real-time control over targeting, bidding, and measurement without reliance on third-party service providers. Large enterprises across Europe are increasingly adopting in-house programmatic platforms to enhance transparency, cost efficiency, and agility in campaign execution. Self-served solutions have been shown to reduce media procurement costs compared to managed service models. Additionally, regulatory pressures under GDPR have incentivized brands to centralize data within their own secure environments, which is further boosting demand for proprietary or licensed advertising technology stacks. The scalability and auditability of software-based solutions make them indispensable for multinational campaigns across fragmented European markets, which is also contributing to the growth of the solutions segment in the European market.

The services segment is projected to grow at the fastest CAGR of 11.9% over the forecast period,d owing to the growing complexity of privacy-compliant campaign execution. As regulatory and technical landscapes evolve, many advertisers lack the internal expertise to navigate cookieless targeting, consent management, and cross-channel attribution. Brands across Europe are increasingly relying on external specialists to implement privacy-preserving advertising strategies. Service providers now offer specialized consulting on contextual targeting, first-party data onboarding, and AI-driven media planning capabilities that are difficult to replicate in-house. Agencies in markets such as France and the Netherlands have developed proprietary contextual classification engines that deliver strong accuracy in brand-safe placement, as validated by independent auditors. This expertise gap is expected to boost the expansion of the services segment in the European market.

By Type Insights

The search advertising segment accounted for the major share of 51.8% of the European market in 2024, owing to the high commercial intent of search queries drives conversion efficiency. Search advertising thrives on user-initiated queries that signal immediate purchase interest, which makes it uniquely effective for performance marketing. According to Google’s Economic Impact Report for Europe released in January 2025, businesses earned an average of 6.20 euros in revenue for every 1 euro spent on Google Search Ads across the EU in 2024. This return is particularly strong in sectors like travel, insurance, and electronics, where decision-making is sresearch-intensivee. According to Eurostat, 78% of Europeans used search engines to compare products or services before purchasing in 2024, which is creating a vast pool of high-intent traffic. Moreover, the integration of shopping ads and local service listings has expanded search advertising beyond text into visual and transactional formats. Many small businesses in Germany reported that search ads generated their highest quality lead, and this confirms their importance in driving qualified customer engagement. This direct link between user intent and advertiser outcomes is primarily contributing to the dominance of the search advertising segment in the European market.

The banner advertising segment is anticipated to progress at a CAGR of 9.88% over the forecast period, owing to the resurgence through native and contextual integration. Traditional banner ads have been revitalized through native placements that blend seamlessly into editorial or social feeds, which is reducing ad blindness. According to the European Brand Safety Council, native banner formats achieved a 5.2% average click-through rate in 2024 compared to 0.45% for standard display banners. Publishers like Le Monde, Der Spiegel, and El País now offer premium native inventory that aligns with content themes to enhance relevance and trust. Contextual banner campaigns targeting sustainability or health topics have shown notably higher engagement, reflecting how editorial alignment transforms banners from interruptive elements into value-adding content and propels the expansion of the banner advertising segment in this regional market.

COUNTRY ANALYSIS

Germany Digital Advertising Market Analysis

Germany dominated the digital advertising market in Europe in 2024 with 23.7% of the regional market share. The robust digital economy, high internet penetration, and strong e-commerce foundation are majorly driving the German digital advertising market. The advertising ecosystem of Germany benefits from a mature tech infrastructure and a population highly receptive to digital innovation. According to the German Federal Statistical Office, 96% of households had internet access in 202,4, with 89% engaging in online shopping annually. Digital adspendings continued to grow as automotive, finance, and retail sectors invested heavily in performance marketing. Many large enterprises in Germany have adopted customer data platforms as part of their compliant first-party data strategies. This regulatory clarity, combined with economic scale and digital literacy, is significantly contributing to the dominating role of Germany in the European digital advertising market.

United Kingdom Digital Advertising Market Analysis

The United Kingdom is another major market for digital advertising in Europe and held the second biggest share in 2024. London remains Europe’s ad tech hub and hosts over 400 martech and adtech firms that serve both domestic and international clients. According to Ofcom, 72% of households subscribed to streaming services in 2024, which is enabling rapid growth in addressable TV advertising. According to the Institute of Practitioners in Advertising, the UK market also leads in AI adoption, with 53% of agencies using generative tools for ad creation. Despite regulatory divergence from the EU, the UK’s Information Commissioner’s Office has provided pragmatic guidance on cookie consent that allows innovation to continue. This blend of creative excellence, technological depth, and adaptive regulation is majorly driving the digital advertising market in the UK.

France Digital Advertising Market Analysis

France occupied a prominent share of the European digital advertising market in 2024, owing to the dynamic digital media landscape and aggressive investment in video and social advertising. France’s strength lies in its vibrant creator economy and high engagement with short-form video. According to Médiamétrie, 68% of internet users aged 18 to 34 consumed TikTok or Instagram Reels daily in 2024. This has made France a testing ground for influencers and interactive ad formats. The government’s “France Relance” digital transition plan also supported SME adoption of programmatic tools through various digitalization grants. Additionally, French broadcasters like TF1 and M6 have pioneered hybrid addressable TV models that combine linear and digital inventory. These structural and cultural factors propel France as a high-growth, innovation-led market within Europe.

Italy Digital Advertising Market Analysis

Over the forecast period. Italy is anticipated to record a notable CAGR in the European digital advertising market due to the accelerated digital transformation following pandemic-driven behavioral shifts. Digital ad expenditure in Italy significantly increased in 2024. Southern Europe’s late but rapid e-commerce adoption has been a key catalyst. Online retail sales saw year-on-year growth in 2024. This surge has pulled advertising budgets toward performance channels, with search and social ads expanding annually. Mobile penetration is particularly influential; many Italians access the internet primarily via smartphones, which is making mobile video and in-app advertising highly effective. Local platforms like Subito and Banzai have also developed native ad solutions tailored to Italian consumer preferences. While historically lagging in digital maturity, the Italian market is now characterized by high velocity growth and increasing sophistication in data-driven marketing.

Spain Digital Advertising Market Analysis

Spain is estimated to witness a healthy CAGR during the forecast period in this regional market, owing to its mobile-first consumer base and strong regional media fragmentation. According to a report by IAB Spain, digital ad spending in Spain in 2024 rose significantly, and Spain leads Europe in mobile internet usage, with users spending an average of several hours daily on smartphones. This behavior has made in-app advertising and location-based campaigns exceptionally effective, particularly in tourism and retail. The country also exhibits high social media engagement, with 70% of Spaniards using Instagram or Facebook daily, creating fertile ground for social commerce. Regional publishers in Catalonia and Andalusia have developed localized programmatic marketplaces that cater to linguistic and cultural nuances, which is enhancing ad relevance. These hyperlocal and mobile-centric dynamics position Spain as a resilient and adaptive market within the European digital advertising market.

COMPETITIVE LANDSCAPE

Competition in the Europe digital advertising market is characterized by intense rivalry among global technology giants, specialized ad tech firms, and emerging retail media networks. Dominant players leverage scale, data assets, and integrated ecosystems to maintain advantage, while niche providers differentiate through privacy-compliant solutions, contextual targeting, and vertical-specific expertise. Regulatory complexity acts as both a barrier and a catalyst—discouraging smaller entrants yet creating opportunities for compliant innovation. The shift toward cookieless environments has intensified investment in identity resolution alternatives and first-party data strategies. Simultaneously, the rise of connected TV and retail media has fragmented demand, compelling players to diversify offerings. Price competition remains moderate due to performance-based pricing models, but differentiation hinges on transparency, brand safety, and measurable ROI. This dynamic landscape fosters continuous technological adaptation and strategic consolidation, ensuring the market remains both contested and innovative.

KEY MARKET PLAYERS

A few of the market players in the Europe digital advertising market include

- Adobe

- Amazon.com Inc.

- AOL (Yahoo)

- Baidu

- ByteDance

- Dentsu Inc.

- Disruptive Advertising

- IAC

- Meta

- Microsoft Corporation

- Tencent Holdings Ltd.

- Verizon

- WebFX

- X Corp. (formerly Twitter Inc.)

Top Players In The Market

- Google operates as a foundational force in the Europe digital advertising market through its integrated ecosystem of search, YouTube, Display Network, and programmatic tools. The company enables precise audience targeting while navigating Europe’s stringent data regulations through privacy-focused innovations like the Privacy Sandbox. In early 2025, Google expanded its certified measurement partnerships with European broadcasters to enhance cross-platform attribution. It also launched new AI-driven creative optimization features for European advertisers, allowing dynamic ad generation compliant with regional data laws. These initiatives reinforce its role in shaping performance and brand advertising standards across the continent while maintaining its global leadership in digital ad technology and infrastructure.

- Meta Platforms exerts significant influence in Europe through its social advertising channels, including Facebook, Instagram, and WhatsApp. The company has prioritized adapting its ad targeting systems to align with GDPR and evolving cookieless standards. In late 2024, Meta introduced advanced contextual targeting tools for European markets and enhanced its Advantage+ shopping campaigns with localized language and payment integrations. It also deepened collaborations with European e-commerce platforms to streamline conversion tracking without relying on third-party identifiers. These actions demonstrate Meta’s commitment to sustaining advertiser performance while adhering to Europe’s unique regulatory and consumer privacy expectations, reinforcing its global position in social and performance advertising.

- Amazon Advertising has rapidly expanded its footprint in Europe by leveraging its e-commerce dominance and first-party shopping data. The company offers highly effective retail media solutions that connect brands directly with consumers during active purchase journeys. In 2024, Amazon launched localized ad formats in Italy and Spain and integrated its demand side platform with major European agency trading desks. It also introduced AI-powered forecasting tools for European advertisers to optimize budget allocation across search, display, and streaming TV. By focusing on measurable outcomes and brand safety within its closed ecosystem, Amazon strengthens its appeal to both global and regional brands, contributing significantly to the evolution of performance-driven digital advertising worldwide.

Top Strategies Used by the Key Market Participants

Key players in the Europe digital advertising market prioritize regulatory compliance through privacy-centric targeting solutions that align with GDPR and ePrivacy standards. They invest heavily in artificial intelligence to automate creative generation, audience segmentation, and bid optimization while minimizing reliance on personal data. Strategic partnerships with local publishers, broadcasters, and e-commerce platforms enable access to premium inventory and first-party data. Companies also expand retail media networks to capture high-intent shoppers within closed ecosystems. Continuous innovation in measurement frameworks—such as attention metrics and incrementality testing—enhances campaign accountability. Additionally, they localize ad formats and payment integrations to address cultural and linguistic diversity across European markets. These strategies collectively strengthen market positioning while ensuring scalability and trust in a complex regulatory environment.

RECENT MARKET NEWS

- In March 2024, Google announced the full rollout of its Privacy Sandbox APIs to all Chrome users in the European Economic Area, enabling interest-based advertising without third-party cookies and strengthening its Europe digital advertising market presence.

- In October 2024, Meta Platforms launched localized Advantage+ shopping campaigns with integrated payment options for small businesses in France and Germany, enhancing conversion tracking while complying with regional data laws and strengthening its Europe digital advertising market presence.

- In January 2025, Amazon Advertising introduced AI-powered budget forecasting tools for European brands and expanded its retail media network to include localized ad formats in Italy and Spain, strengthening its Europe digital advertising market presence.

- In July 2024, Microsoft Advertising integrated its Microsoft Audience Network with leading European news publishers through a contextual targeting partnership, expanding brand-safe display inventory and strengthening its Europe digital advertising market presence.

- In November 2024, TikTok for Business launched a GDPR compliant measurement solution in collaboration with European verification vendors, enabling accurate campaign attribution without personal data and strengthening its Europe digital advertising market presence.

MARKET SEGMENTATION

This research report on the Europe digital advertising market is segmented and sub-segmented into the following categories.

By Platform

- Computer

- Smartphone

- Others

By Format

By Offering

By Type

- Search Advertising

- Banner Advertising

- Video Advertising

- Social Media Advertising

- Native Advertising

- Interstitial Advertising

By End Use

- BFSI

- Automotive

- IT & Telecommunication

- Healthcare

- Consumer Electronics

- Retail

- Media & Entertainment

- Education

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

link